How Much More Will Cities and Counties Pay CalPERS?

When speaking about pension burdens on California’s cities and counties, a perennial question is how much are the costs going to increase? In recent years, California’s biggest pension system, CalPERS, has offered “Public Agency Actuarial Valuation Reports” that purport to answer that question. Notwithstanding the fact that CalPERS predictive credibility is questionable – i.e., they’ve gotten it wrong before – these reports are quite useful. Before delving into them, it is reasonable to assert that what is presented here, using CalPERS data, are best case scenarios.

In partnership with researchers at the Reason Foundation, the California Policy Center has compiled the data for every agency client of CalPERS, including 427 cities and 36 counties. In this summary, that data has been distilled to present two sets of numbers – payments to CalPERS for the 2017-2018 fiscal year, and officially estimated payments to CalPERS in the 2024-25 fiscal year. In calculating these results, the only assumption we made (apart from the assumptions made by CalPERS), was for estimated payroll costs in 2024. We used a 3% annual growth rate for payroll expenses, the rate most commonly used in official actuarial analyses on this topic.

So how much more will cities and counties have to pay CalPERS between now and 2024? How much more will pensions cost, six years from now?

On the table below, we provide information for the 20 cities that are going to be hit the hardest by pension cost increases. To view this same information for all cities and counties that participate in the CalPERS system, download the spreadsheet “CalPERS Actuarial Report Data – Cities and Counties.”

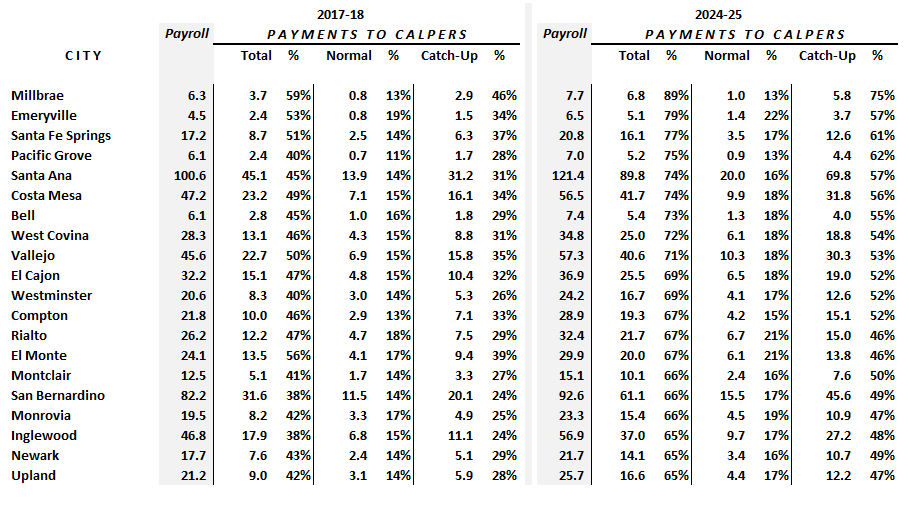

CalPERS Actuarial Report Data

The Twenty California Cities With the Highest Pension Burden ($=M)

If you are a local elected official, or if you are an activist, journalist, or anyone else with a keen interest in pensions, these tables merit close scrutiny. Because they not only show costs estimates today, and seven years from now, but they break these costs into two very distinct areas – the so-called “normal” costs, which are how much employers have to pay into the pension fund for current workers who are vesting one more year of future benefits, and the “catch-up” costs, which are what CalPERS charges employers whose pension plan is underfunded.

Take the first city listed, Millbrae. By 2024, we predict Millbrae will have the highest total pension payments of any city in California that belongs to the CalPERS system.

The table presents are two blocks of data – the set of columns on the left show current costs for pensions, and the set of columns on the right show the predicted cost for pensions. In all cases, the cost in millions is shown, along with the cost in terms of percent of total payroll.

Currently, as can be seen on the table, for every dollar it pays active employees in base wages, Millbrae must contribute 59 cents to CalPERS. This does not include payments to CalPERS that Millbrae collects from its employees via withholding. The same data show that, by 2024, for every dollar Millbrae pays active employees in base wages, they will have to contribute 89 cents to CalPERS. Put another way, while Millbrae may expect its payroll costs to increase by $1.4 million, from $6.3 million today to $7.7 million in six years, their payment to CalPERS will increase by $3.1 million, from $3.7 million today to $6.8 million in 2024.

But here’s the rub. Nearly all of this increase to Millbrae’s pension costs are the “catch-up” payments on the city’s unfunded liability. In just six years Millbrae’s payment on its unfunded liability will increase by 99%, from $2.9 million today to $5.8 million in 2024.

Why?

What are the implications?

It is difficult to overstate how outrageous this is. Here’s a list:

1 – Virtually every pension “reform” over the past decade or so has exempted active public employees from helping to pay down the unfunded liability via withholding. Instead, their increased withholding – in some cases supposedly rising to “fifty percent of pension costs” (the PEPRA reforms) – only apply to the normal contribution.

2 – In order to appease the unions who, quite understandably, lobby for the lowest possible employee contributions to pension funds, the “normal cost” is calculated based on financially optimistic projections. The less time an actuary predicts a retiree will live, and the more an actuary predicts investments will earn, the lower the normal contribution.

3 – In order to cajole local elected officials to agree to pension benefit enhancements, the same overly optimistic, misleading projections were provided, duping decision makers into thinking pension contributions would never become a significant burden on cities and counties, and by extension, taxpayers.

4 – Because cities and counties couldn’t afford to pay down the growing unfunded liabilities attached to their pension plans, tricky accounting gimmicks were employed, where minimal catch-up payments were made in the present in exchange for bigger catch-up payments in the future. The closest financial analogy to what they did would be the “negative amortization” mortgages that were popular prior to the housing crash of 2008.

5 – The consequence of this chicanery is that today, as can be seen, catch-up payments on the unfunded liability are typically two to three times greater than the normal contribution. And it’s getting worse. In 2024, Millbrae, for example, will have a catch-up contribution that is nearly six times as much as their normal contribution.

6 – When a normal contribution isn’t enough, and the plan becomes underfunded, the level of underfunding is compounded every year because there isn’t enough money in the fund earning interest. The longer catch-up payments are deferred, the worse the situation gets.

Yet the normal contribution has always been represented as all that should be required for pension plans to remain fully funded. Just how bad it has gotten can be clearly seen on the table.

Take a look at Pacific Grove, fourth on the list of CalPERS cities with the highest pension burden. Pacific Grove is already paying 40 cents to CalPERS for every dollar it pays to its active employees. But in six years, that amount will go up to 75 cents to CalPERS per dollar of salary to active employees. And take a look at where the increase comes from: Their catch-up payment goes from 1.7 million to $4.4 million in just six years.

Why?

Why isn’t Pacific Grove paying more, now, so that it can avoid more years of having too little money in its pension plan, earning interest to properly fund future pensions? The reason is simple: Telling Pacific Grove to go out and find another $2.7 million, right now, is politically unpalatable. In six years, most of the local elected officials in Pacific Grove will be gone. But where is Pacific Grove going to find this kind of money? Where are any of California’s cities and counties going to find this kind of money?

One final point: These pension plans are underfunded after a bull market in stocks has doubled since it’s last peak in June 2007, and has nearly quadrupled since it’s last low in March 2009. When stocks and real estate have been running up in value for eight years, pension plans should not be underfunded. But they are. CalPERS should be overfunded at a time like this, not underfunded. That bodes ill for the financial status of CalPERS if and when stocks and real estate undergo a downward correction.

CalPERS, and the public employee unions that dominate CalPERS, have done a disservice to taxpayers, public agencies, and ultimately, to the individual participants who are counting on them to know what they’re doing. They were too optimistic, and the consequences are just beginning to be felt.

* * *