Pension Funds, Meet the “Super Bubble”

Earlier this month, outgoing California Governor Jerry Brown predicted “fiscal oblivion” if California’s state and local agencies are not granted more flexibility to modify pension benefits. As if to help Governor Brown make his point, U.S. stock indexes took an obliging plunge. The Dow Jones average cratered in December, dropping nearly 16 percent in three weeks, from 25,826 on December 3rd to a low of 21,792 on December 24th. And whither hence? Nobody knows.

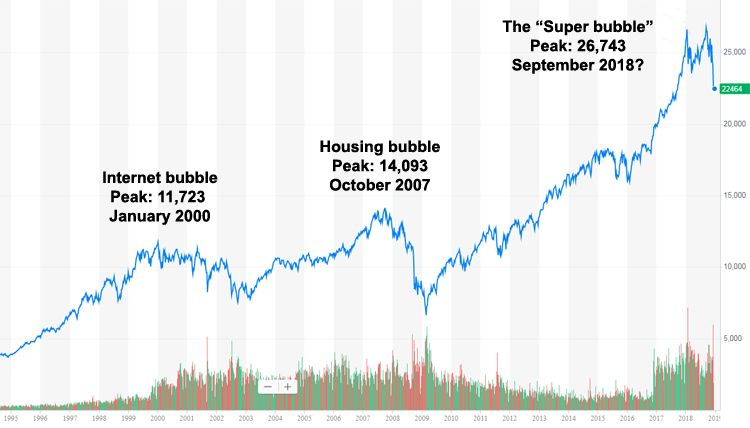

If history and trends are any indication, however, “up” is unlikely. Depicted on the chart below is the performance of the Dow Jones Index from 1995, when the markets began first showing signs of “irrational exuberance,” to the extremely exuberant present day. Clearly shown are the past two bubbles, the internet bubble of 2000, the housing bubble of 2007, and what we may call the “super bubble” or “everything bubble” of 2018.

Dow Jones Stock Index – 1995-2018

It doesn’t take an economist to notice a pattern here. The Dow Jones Index, which tracks closely with all publicly traded equities in the U.S., more than doubled in the four year heady runup to its January 2000 peak, than went into decline for nearly four years, before doubling again between 2004 and 2007. Then when the housing bubble popped, the Dow went off a cliff, dropping to half its 2007 peak in little over a year. In the ten years since 2009, the Dow has exploded again, tripling to a high of 26,743 in September 2018. What now? Visually, at least, another correction is past-due.

There are all kinds of economic reasons why what is visually indicated on the above graph is exactly what’s going to happen. At best, we may hope for stocks to merely stop going up, which is sort of what happened after the internet bubble popped. But what’s different this time?

One key difference is that this time, lowering interest rates is not an option. In January 2000 the Federal Funds rate was 5.5 percent. By June of 2003 it had dropped to 1.0 percent. When interest rates drop, stocks become relatively better investments than fixed rate investments. Lower interest rates also induce more people to borrow, creating liquidity, stimulating consumer spending, which helps corporate earnings which drives up stock prices. The cause and effect is reflected in the stock market history – by 2003, after lowering interest rates by 4.5%, the stock market finally began to recover.

In October 2006 the rate had risen to 5.25 percent. In September 2007, as home sales were starting to drop, it was lowered to 4.75 percent. When the housing bubble popped, and the stock market crashed, the Federal Reserve responded by steady lowering of the Federal Funds Rate. By December 2016 it had dropped to 0.25 percent, the lowest rate possible. What should be of concern, is that the rate today, 2.5 percent, is only half as high as it was during the past peaks. During the previous two bull markets, the Federal Reserve was able to bounce the rate up to around 5 percent before the bears came calling. This time, assuming we’ve hit the peak, only half that increase, to 2.5 percent, was achievable.

A consequence of low interest rates is more borrowing, which is a good thing if that borrowing stimulates economic growth that translates into investments in productivity. But borrowing has not been used to stimulate productive investments. Instead, much of the corporate borrowing over the past decade has been used to finance stock buy-backs. This is a dangerous strategy, causing short-term growth in earnings per share, but loading debt onto corporate balance sheets that will have to be refinanced at interest rates that are increasing, at the same time as investment in research and modernizing plant and equipment has been neglected.

In recent years, borrowing has also been an overused tool of government, starting with the federal government. Federal borrowing accelerated in mid-2008, and hasn’t slowed down since, climbing to over $21 trillion by the 3rd quarter of 2018. As interest rates rise, servicing this debt will become far more difficult. Meanwhile, all U.S. credit market debt – government, corporate, and consumer – has continued to increase. After dipping slightly to $54 trillion in the wake of the burst housing bubble, it was up to a new high of $68 trillion by the end of 2017.

When interest rates fall, not only is the stock market stimulated. Bonds make payments at fixed rates, so when the market rate drops, the price of these bonds increases, since they can be sold for whatever price will give the buyer the same return as the current market rate. Interest rate reductions also cause housing prices to rise, since when interest rates are low, people can afford bigger mortgages since they will be making lower monthly payments. The opposite is also true, which is unfortunate for investors. All else held equal, rising interest rates means lower prices for bonds and housing.

What does this mean for pension funds?

When the super bubble pops this time, all assets will drop in value. Everything pension funds are invested in, equities, bonds, and real estate, will all drop in value. Even if extraordinary measures are taken to stop the decline – such as the fed purchasing corporate bonds – there will be nowhere to run. Public sector pension funds have not prepared for this day of reckoning. CalPERS, for example, in its most recent financial statements was only 71% funded. That would be ok at the end of a bear market, but at the end of a bull market, that is a disaster waiting to happen.

As it is, using CalPERS as an example, government agencies are going to have to nearly double their annual payments. The primary reason for this increase appears to be so the participating agencies will eliminate their unfunded liability on a 20 year repayment schedule. To-date, agencies were making those repayments on a 30 year term, and using creative accounting to minimize the payment amounts in the early years. CalPERS does not appear to have lowered the amount they are expecting their investments to earn, and this is critical. Because while they have lowered their expected rate of return to “only” 7.0 percent, they have also quietly lowered their long-term assumed inflation rate. This means they are still relying on nearly the same real rate of return for their investments.

When the super bubble pops, the challenges facing pension funds will not be the only economic problem facing Americans. Unwinding the debt accumulated during a credit binge lasting decades will impact all sectors of the economy. The last thing the fragile finances of government agencies will need is even higher required contributions to the failing pension funds. Instead those running these pension systems need to try new approaches, including modifying benefit formulas, but also redirecting investments into local infrastructure projects – projects that not only create jobs, but address practical and urgent goals such as building resilient, upgraded backbones for supplying water, energy, and transportation.

In early 2019, the California Supreme Court is about to issue one of its most consequential rulings ever, in the case CalFire Local 2881 vs. CalPERS. It is possible this ruling will grant government agencies (and voters) more flexibility to modify pension benefits. Such an opportunity cannot come too soon, if fiscal oblivion is to be avoided when the super bubble finally pops.

* * *